The cost of being a teen

For many high school seniors, the college admissions process is supposed to be exciting. But for a growing number of students, the first symbol of independence has launched them headfirst into adulthood where students are now forced to make decisions that may set them decades into debt before they even set foot on a campus.

This is the price of higher education and it’s shaping the way many students are thinking about their futures.

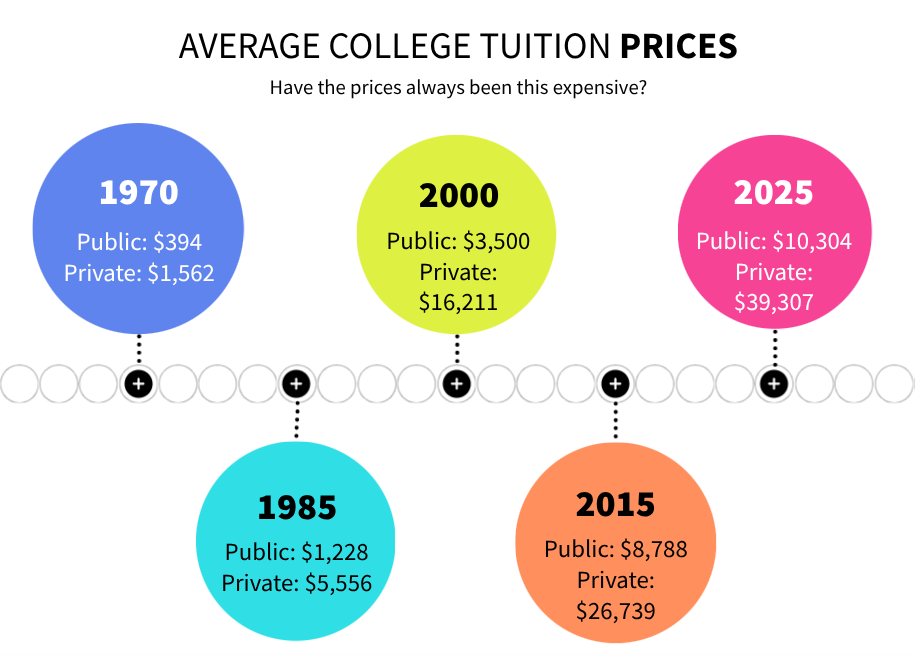

Over the past three decades, the price of college education has exploded. According to the College Board, average yearly tuition at public four-year colleges and universities jumped from roughly $4,900 to nearly $11,000 after adjusting for inflation. At private institutions, average tuition doubled from $19,000 to $38,000. While those numbers represent averages, the price at some schools is now pushing $100,000 a year when room, board, and fees are factored in.

Why have the prices jumped? Decades ago, public colleges used to be mostly funded by the government with states covering 75% of costs. Today, it is closer to 50/50, placing more pressure on the students to cover the rest. The Great Recession made things worse as states cut billions from higher education budgets, resulting in colleges raising tuitions. By 2018, public colleges were receiving $6.6 billion less from states than before the crash. At the same time, middle-class salaries have barely budged in four decades, keeping millions of families stuck between rising costs and stagnant pay checks.

What often gets overlooked is the financial burden before a student even commits to a school. Application fees run between $50 to $100 per school and during the 2024-2025 cycle, Common App users applied to an average of 6.14 colleges— translating to roughly $295 in application fees alone. This is before factoring in SAT or ACT registration fees, campus visit expenses, and more which can exceed $2,500.

While many students may have gathered savings or support from their families, some seniors are navigating the financial process on their own.

“Application fees have definitely stopped me,” said Anna Bardunias (‘26). “There were a lot of schools I wrote supplementals for that I ended up not applying to because they were ‘risk’ schools. I ended up not applying to these risk schools because if I did get in, I knew I probably wouldn’t be able to [afford them] anyways— so that was gonna make me more upset than just not knowing.”

Bardunias got into Northeastern, but the excitement was brief after realizing they offered her little to no money.

“I got into the Boston campus and I was so excited, but I cannot afford to go there. So it’s almost like a backhanded compliment— “we want you, but we’re not giving you any money.”

Getting into college has spawned an entire economy. Private SAT tutors charge anywhere from $50 to $300 per hour, with elite specialists charging $1,000 or more. Comprehensive test prep packages can run from $1,500 to $6,000 or higher. The private college counseling industry pulled in $3 billion in revenue in 2024 alone, according to market research firm IBISWorld.

For the students who can’t afford these services, they are left to navigate the system on their own. At East, the guidance counselor to student ratio is around 220 students to 1 counselor, leaving many students at a disadvantage.

Justin Forstadt (‘26), who is applying simultaneously with his twin brother while two older sisters have already gone through four-year universities, found the paid guidance from a college advisor he received to be underwhelming.

“I would say my college advisor was a dumb financial investment… For me, I would say do your research on your own to decide what you want.”

His family is one of many trying to spread limited resources across multiple applications and as a result has capped the amount of schools Forstadt applied to.

“My parents wanted [my brother and I] to apply to about 8-10 schools since there is a cost to apply with each,” said Forstadt.

For the students who do get into colleges and receive scholarship aid, the financial picture can be disorienting. Once students do the math, the tuition price is still daunting.

Bardunias talked about what sounded like a substantial offer from Drexel University.

“I ended up getting a larger scholarship that I thought was gonna pay for at least half of my tuition. Then, you see how much more expensive it is,” said Bardunias. “I opened it and was like, ‘Oh my god, $40,000— it sounds amazing!’ And then you look farther and you realize, “No, the whole tuition is actually over $100,000 and I would still have to pay over $60,000.”

Bardunias also described a “FAFSA cliff”, a frustrating sector where her family’s income disqualifies her from federal aid, but there are no savings for her education either.

“I don’t qualify for FAFSA, but my parents aren’t giving me money… It kind of sets you up in a weird, awkward position because a lot of people do have money saved from their childhood,” said Bardunias.

Even for the students who have savings, the daunting price doesn’t alleviate much pressure.

“Finances have definitely affected where my parents want me to go because they don’t want me to end up in a pile of student loans after my four years,” said Ty Ramella (‘26) who has a college fund.

Arguably, the most disappointing consequence from the high priced college admissions process is the way it bends students’ futures before they’ve even started. Students are now choosing schools, majors, and career paths not based on passion, but rather what they can realistically afford to pursue.

Bardunias, who wants to go pre-med and attend medical school, found herself making decisions that will impact herself years down the road.

“I could spend more money for undergrad and go out of state for four years, which is something I personally wanted to do. But inevitably I would end up needing so much money for med school— it would not make financial sense.”

Forstadt, watching his sister struggle after completing a journalism degree, has turned to business as his intended major.

“My sister is a journalist, so her major was journalism. She makes pretty much nothing in today’s market. So I would say it has affected what I want to do in college and the place I’m looking to work after college.”

Ramella remains convinced that college is worth it, but acknowledges the system is broken.

“I was definitely bewildered by the fact that the price is so absurd nowadays— and the fact that colleges can get away with charging these insane prices. Some of them do not even have a relatively similar return on investment to the price you’re paying.”

The promise and dream of a higher education is still there, but for many students they know the choice they make now will hold weight on them for years to come. The question is no longer just “Where do you want to go?” It’s “What can you afford to want?”

Being a student today is not easy, and that can often be overlooked. With pressure coming from all different aspects of life, teens face daily problems greater than just schoolwork. Many are balancing sports, advanced classes, extracurriculars, and life outside of school all at the same time — all coming at a cost. The balance comes with a cost that is related to both money and time and energy.

Dylan Kratchman (‘27) is a true all-around athlete. She plays a different sport each season of the year: soccer in the fall, basketball in the winter, and softball in the spring. Her day rarely ends at the sound of the school bell.

After practice, she still has homework waiting. Most days follow that similar routine, which leaves little time to fully relax.

She spends around two hours a day on sports, which adds up over a long and demanding week. During certain times of the year specifically when seasons overlap, her schedule becomes even more intense. She described going from one sport straight into another, sometimes in the same day.

“Sports are kind of my escape from school,” she said.

Even so, that schedule comes with sacrifices. Free time is limited, and sometimes the only thing she wants is a break with nothing planned.

Along with the time commitment, sports can also come with real costs. Students often have to pay activity fees to play, along with equipment, travel, and training. The Cherry Hill East Sports Activity fee cost $80 per student athlete and the remainder of the costs vary per sport. For many families, those expenses add up quickly over the course of a season.

For Rivi Jay (’26), the pressure looks different. Her focus is on academics and leadership. She is taking four AP classes while also leading the Autism Acceptance Club.

“I spend a lot of time doing schoolwork for all those classes,” she said.

The workload changes depending on the class. AP Literature, for example, involves long reading and writing assignments that take up a lot of her time. She also spends part of each week preparing for her club. That includes making presentations and promoting meetings.

“So maybe an hour each week… but then like for April, definitely a couple more hours,” she said.

Even without major fees tied to her classes, being a student still comes with expenses. AP exams cost $99, and even something as simple as a parking pass at East requires a fee of $50. Her club is also working on a t-shirt fundraiser, which brings in additional costs.

Balancing everything can feel overwhelming at times.

“Yes, but I have figured out a lot of methods to make it less overwhelming,” she said.

She stays organized and focuses on her priorities instead of trying to do everything at once.

These students’ experiences show that the cost of being a teen goes beyond what shows up on a bill. It shows up in packed days filled with practices and club meetings after school, late nights studying for multiple tests, and the constant pressure to keep up while trying to become the person you want to be. The challenge is not just doing everything, but learning how to manage it without burning out.

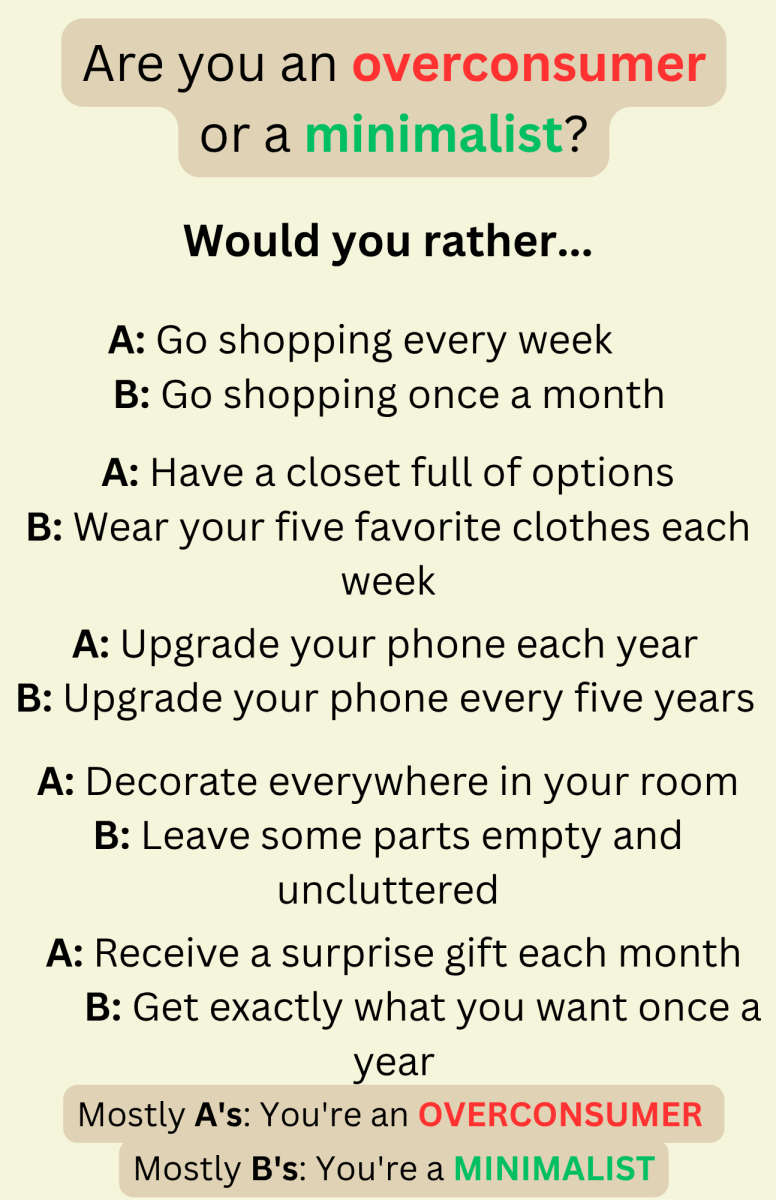

When it comes to cost efficiency and sustainability, Gen Z can be contradictory. Overconsumption and minimalism are both popular social media trends that have exploded over the past 10 years, but what happens when one of them is good for your wallet while the other breaks the bank?

Overconsumption

It might not be obvious at first glance, but social media has become a space that is driven by sales and marketing. When you break down what the word influencer actually means, it raises questions about your favorite content creator’s true motivations. Many popular influencers are being paid by companies to influence their audience to subscribe to a service or buy a product. Platforms like YouTube and TikTok have made undisclosed ads illegal— meaning influencers have to clearly declare to their followers when they’re promoting something for a sponsor. Despite this, it can be hard to avoid the bombardment of products that content creators peddle. There are creators who base their entire account on shopping “haul” videos, where they show off hundreds of dollars worth of stuff they’ve purchased over the week. Others display drawers and drawers of makeup they’ve been sent for free in exchange for promotion. According to a study done by ConsumerAffairs, 67% of Americans have bought something they saw on social media, likely because an influencer convinced them they needed it.

Alongside influencer pressure, TikTok has the TikTok Shop feature, which is the platform’s way of competing with fast fashion companies.

“TikTok Shop has really cheap, really suspicious stuff and feels like Shein. When it first came out, every single video on my For You Page turned into an ad,” said Aria Roy (‘27). “They make you think that if you don’t buy things at that moment, at that time, you’ll never get it. And then you think why did I buy that? I’m never using this ever.”

Young people are being shown excessive amounts of products and taught to believe that’s normal. They’re constantly attacked by advertisements from influencers and social media platforms. It’s easy for them to want to spend their money on cheap items from Shein and TikTok Shop, but those hauls add up. Teens partaking in social media overconsumption culture are overspending on things they don’t need.

Minimalism

On the opposite side of social media, the minimalism trend has taken off. This is not to be confused with the “clean-girl aesthetic,” which is an example of consumerism under a minimalist mask. There is an overwhelming amount of skincare, makeup, and hair products that clean girls and guys buy in order to fit the mold. Real minimalists are practicing recent trends like taking the brand logos off of products so they aren’t as tempted to buy them again.

Some teens also care a lot about the environment. Minimalists try to reduce the plastic waste that comes from overconsumption, because it will inevitably end up in landfills. This boils down to not buying multiple products where you only need one.

East’s Environmental Club recently had a sustainable makeup event, where participants could use environmentally friendly materials to make natural toner. Little things like these are enough to reduce overconsumption and therefore spending, even if it may not feel like it.

Reducing the time spent online shopping will also lessen the urge to get every possible discount. It might also make shopping in-store more appealing.

“I trust the stuff that I see in real life more than what I see online,” said Jack Slater (‘27). “What you see on social media could be totally different than what you get in real life.”

Minimalism isn’t necessarily better than overconsumption, it’s all about finding a balance that works for the individual. If buying every shade of lipgloss fits comfortably within the budget, the debate becomes moral, not financial. Teens simply need to make sure they don’t buy beyond their means just to follow a trend.

In 2004, Utah became the first state to mandate a financial literacy class as part of high school graduation requirements. Over the past 20 years, more and more states have followed this trend. As of October 2025, 30 states require some type of personal finance course in order to graduate.

New Jersey officially made financial literacy education mandatory in 2019, though there have been lesser requirements for certain grades in the state as early as 2015.

At Cherry Hill High School East, Financial Literacy is a half-year course open to juniors and seniors as a graduation requirement.

The curriculum for Financial Literacy, or Fin Lit as it is often abbreviated, consists of higher education expenses, college tuition, car and home buying, investing, banking, and budgeting.

Ms. Aimee Hird is one of the handful of East teachers who offered to teach the course when it was first introduced in the district. She was selected because of her business certification, seeing as business and finance are closely intertwined.

When asked to compare Fin Lit at East with other schools around the country, Hird mentioned how relevant the East curriculum is.

“We like to talk about real life things. We talk about the FAFSA and we help with taxes. Other places just have a website that provides them slideshows and EdPuzzles. We use the website too, it has a wealth of material, but our discussions about real life make the program better,” Hird said.

The FAFSA stands for the Free Application for Federal Student Aid, and any students looking to attend college in the next year have to fill it out in October in order to receive financial aid. Because it has the potential to drastically alter one’s college experience, East students are receiving vital information in their Fin Lit courses. Beyond college, knowing these financial tricks for any facet of life can put students ahead.

The question becomes, is the course actually making an impact on kids’ financial knowledge?

Hird believes it varies, saying, “I think it makes an impact, but not on everybody. Some students are too young and they’re not thinking about money. There are other students that are trying to get ahead though.”

She notices how those ambitious students will show active interest in discussions about investing or taxes, often having investment accounts, cars they need to budget for, or jobs of their own.

Talking about real life situations is what gets students interested, according to Hird. It shows them that the discussions they have in the classroom can be applied to their own lives to strengthen their financial knowledge and improve their spending habits.

Next year, Fin Lit will be offered as half of a new course called AP Business with Personal Finance, while the other half will be Entrepreneurship. This will be a way for students to fulfill their graduation requirements while simultaneously taking both a business course and an AP course. Hird has a feeling this class will be very popular at East.

Financial Literacy might not resonate with every student, but it provides a valuable head start for those who are eager to start thinking about the quickly approaching future.

Walking into your activity, knowing you paid for your participation yourself, it can change your entire perspective. It is no longer just another activity, something you feel pressured to do because your parents pushed you into it at a young age. You no longer believe that participation is expected of you. It is something you chose for yourself. Something you earned. Taking on the costs of AP exams, sports and activity fees, and extracurricular activities increases the meaning behind these activities, giving students a purpose and clear sense of motivation in what they are doing.

At first, these expenses were an inconvenience. School is supposed to be free for students, providing them equal access to activities and opportunities. That said, there’s no denying that not all students have the same ability to afford participation in these activities, and all of the smaller expenses that may not be clear on the surface. But at the same time, there’s a clear effect when you start to take on the responsibility of paying the cost to participate in these activities: everything begins to mean so much more.

When you’ve earned something, whether that is money from a part-time job, a portion of your paycheck, or a recognition of just how expensive these things are, you tend to look at them differently. The Advanced Placement (AP) exam, for example, you’re not just studying and preparing to take a cumulative test at the end of the school year. You are not just going to class each day, coming home and opening a textbook to take your nightly notes on the next chapter of reading. You are doing something for yourself. You are pushing yourself each day to accomplish something with the goal of proving to yourself that you have the power to do so.

You set a goal for yourself, and you are not going to let anyone or anything stand in your way or keep you from achieving that goal.

By funding your activities yourself, it is not making them more expensive, but rather it is making them more valuable and personal. Participation becomes something that has been earned, a reflection of your continued efforts over time. Their participation is not only a real investment in their future, but in their present as well.